Credit Union Data 101 – How CDO can harness Risk Analytics, Marketing Analytics and Portfolio Analytics

In this blog you will discover how Chief Data Officers leverage Risk, Marketing, and Portfolio Analytics to steer credit unions towards growth and stability in an evolving financial landscape.

In today’s data-driven era, the role of a Chief Data Officer (CDO) extends beyond data management to strategic orchestration. The convergence of Risk Analytics, Marketing Analytics, and Portfolio Analytics offers a transformative opportunity for CDOs to shape the future trajectory of their organization. By harnessing the power of these three critical analytics domains, CDOs can steer their institutions toward operational excellence, informed decision-making, and sustainable growth. Let’s explore how a CDO can leverage this triumvirate of analytics to drive impactful outcomes and solidify their organization’s competitive edge.

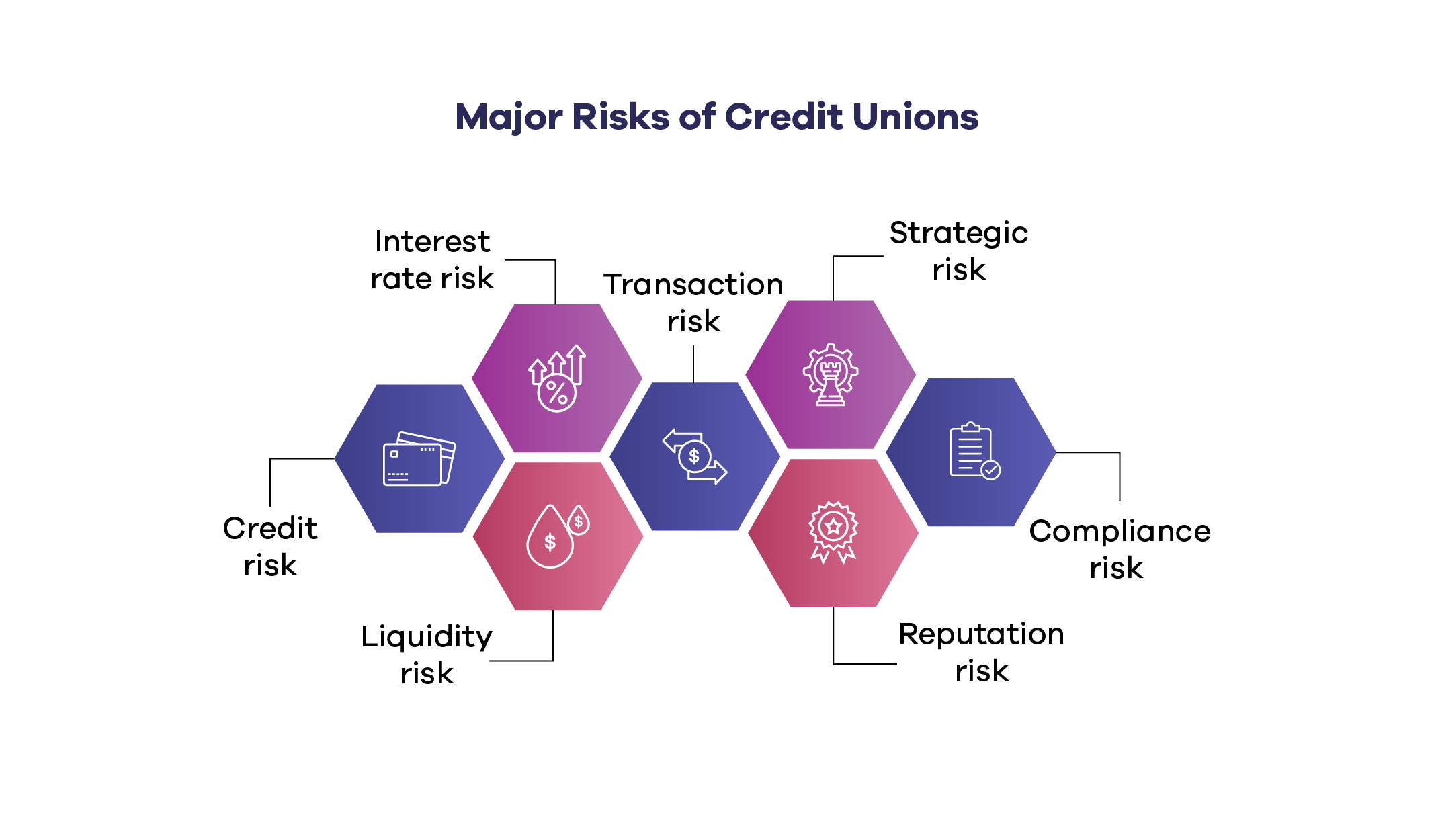

Navigating Risk Factors: Internal and External Concerns for Credit Unions

Credit unions face controllable internal risks like fraud, data breaches, legal noncompliance, and staff/visitor injuries, warranting focused attention.

External risks such as exchange rates, interest rates, natural disasters, and fund loss due to theft, often lie beyond control.

Crafting strategies for external risks can aid credit unions, but complete nullification through risk management is improbable.

Enhancing Credit Union Success through Robust Risk Management

A comprehensive and well-constructed risk management plan offers substantial value to credit unions. It not only ensures a secure environment for staff and members but also shields assets, property, income, and time. Moreover, the presence of risk management strategies diminishes legal liabilities and the looming threat of potential litigation. In an era where credit unions cannot afford to overlook risks, the implementation of effective risk management plans becomes paramount, not only for fortifying operational stability but also for nurturing overall success.

Strategic Integration of Risk Management: A Necessity in Today’s Landscape

In the fast-paced realm of modern business, rapid service and loan decisions have become expectations for customers. To meet these demands, credit unions must embrace advanced technology and online services to cater to their members. Amidst the prevailing market uncertainty, defining the balance between risk and opportunity has become increasingly complex. While generating revenue remains vital, credit unions are cautious about elevated-risk loans, yet they must continue funding loans to sustain their operations.

The solution lies in effective risk management software that optimizes performance, automates processes, and conquers the risk-reward equation. This allows credit unions to not only expand their customer base and revenue but also navigate the intricate market landscape. Elevating efficiency and revenue not only elevates the credit union’s brand but also ensures its sustained growth.

Key Risk Indicators (KRIs): Enhancing Proactive Risk Management

In the realm of risk management, Key Risk Indicators (KRIs) emerge as crucial tools for gauging potential vulnerabilities and early warning signals. Tracking and reporting these KRIs provide invaluable insights into emerging risks and exposures. When a KRI points to a warning sign, the immediate investigation becomes paramount to optimize operational efficiency and mitigate potential risks. Regular and consistent collection of KRI data is essential to extract maximum benefit from this approach.

Take, for instance, the application of KRIs in tracking the volume of loans originated by a credit union over a specific period. This KRI metric serves as a valuable guide in determining optimal mortgage loan amounts based on available capital. KRIs undoubtedly prove effective and useful. Even the slightest oversight could lead to escalated exposure and potential performance setbacks. Hence, meticulous monitoring and proactive utilization of KRIs are imperative to fortify risk management strategies and drive overall success.

Unveiling the Role of Marketing Analytics

In the dynamic landscape of credit unions, the strategic utilization of marketing analytics emerges as a pivotal force. This multifaceted approach empowers credit unions to harness data-driven insights, enabling them to make informed decisions, enhance member engagement, and optimize marketing efforts for maximum impact.

Marketing analytics delves into the depths of member behavior, preferences, and trends, unearthing valuable patterns that shape marketing strategies. By deciphering these insights, credit unions can tailor their offerings to meet member needs, driving satisfaction and loyalty.

In the era of digital transformation, marketing analytics is the compass that guides credit unions toward sustained growth and relevance. As credit unions strive to evolve and remain competitive, leveraging the power of data-driven marketing becomes not just a strategy, but a necessity.

Exploring Customer Journey and Member Experience

Shift the industry perspective from ‘channels’ to consumer-centric banking. Members demand consistent functionality and real-time data, regardless of their chosen access point.

Gaining insight by intersecting customer journeys and experiences is pivotal for a credit union’s future. Utilizing net promoter scores and member data unveils success factors. Engaged members who embrace your offerings can foster growth by expanding interactions and attracting new members.

Marketers need to understand their members’ first-party data, directing efforts toward campaigns and strategies that cultivate enduring customer value.

Elevate Your Credit Union’s Digital Strategy with Strategic Investments

Significant Budget Boosts in Email, Social Media, and Content Marketing. Amid rapid changes, mastering these channels to maintain your financial institution’s prominence is vital. A digital strategy entails not only recognizing digital marketing avenues but also harnessing marketing technology’s potential.

adopted artificial intelligence (AI) as a marketing strategy have seen a 37% reduction in marketing costs and a 39% increase in revenue.

Employing AI enables precise audience targeting, conserving time, resources, and funds for credit unions.

Why Loan Portfolio Analysis Matters

Credit unions require robust tools for seamless tracking and analysis of loan operations, allowing them to gain insights into loan type distribution. Moreover, credit unions routinely assess and mitigate risk levels linked to specific loan categories, like residential versus commercial property loans.

Conducting comprehensive loan portfolio analysis becomes pivotal, as it unveils the credit union’s loan balance strength and diversification, while also guiding tailored marketing approaches for each loan type.

Employing Key Performance Indicators (KPIs) offers a gauge of the credit union’s loan portfolio status across multiple dimensions. This strategic approach ensures credit unions stay agile and informed in optimizing their lending strategies.

Portfolio analytics empowers your organization with a comprehensive range of advantages, spanning from regulatory compliance to dynamic risk assessment and strategic marketing insights. With flexible data integration, precise estimations, and valuable updates, you can elevate your operations and make informed decisions.

Here are a few key benefits of employing Loan Portfolio Analytics:

- Ensuring Compliance with Interagency Appraisal Guidelines

- Real-time Credit Portfolio Monitoring

- Insight into Current and Future Credit Risk Exposure

- Seamless Integration of Data in Various Formats for Database Analysis

- Identification of Cross-Selling and Up-Selling Opportunities

- Regular, Quarterly Valuation Updates for Real Estate and Automobile

Advantages of Loan Portfolio Analysis:

Informed Strategic Planning: Portfolio analytics offer profound insights into credit union portfolio performance, empowering astute decision-making and strategic envisioning.

Proactive Risk Mitigation: Through portfolio data analysis, credit unions can pinpoint potential risks and take preemptive steps to ensure financial stability in their operations.

Strategic Advantage: Harnessing portfolio analytics provides credit unions with a competitive edge, fostering agility, innovation, and adaptability to ever-evolving market trends.

Conclusion

In today’s dynamic financial landscape, the significance of comprehensive analytics for credit unions cannot be overstated. Embracing risk analytics fortifies the foundation of credit unions by identifying potential vulnerabilities, empowering proactive risk management, and ensuring operational resilience. With marketing analytics, credit unions gain a compass to navigate the intricacies of member preferences and behaviors, enabling personalized engagement and targeted campaigns that foster member satisfaction and loyalty. Portfolio analytics, on the other hand, unveils a treasure trove of insights, from optimizing lending strategies to ensuring regulatory compliance, while granting credit unions the foresight needed to remain competitive and strategically agile.

Together, these three pillars of analytics provide credit unions with a panoramic view of their operations, risk exposure, member interactions, and market positioning. In an era of rapid change and heightened member expectations, harnessing the power of analytics isn’t merely a choice; it’s a strategic imperative. By embracing risk analytics, marketing analytics, and portfolio analytics, credit unions pave the way for sustainable growth, operational excellence, and member-centric success, ensuring they are not just prepared for the future, but leading the way.