The Growing Importance of APIs in Banking and Finance

Read on to understand exactly how APIs are gaining steam in the finance world — as well some possible challenges of utilizing these APIs.

APIs are becoming an increasingly important part of banking and finance technology. Today, consumers prefer to bank digitally, with 85% of Americans saying they’d rather bank via a mobile app or a web browser.1 Banks are utilizing these digital mediums not only to better serve their customers, but also to create new revenue streams and gain access to additional customer data. To fully realize these benefits, APIs are needed.

Open banking and APIs explained

Open banking is a trend that is quickly catching on in the banking and finance industries. While it is not yet mandatory in all countries (the US, for example) the goal of the open system is to foster competition among banks and improve the customer experience. Open banking is facilitated by APIs, which enable banking institutions to share their personal financial data with third-party companies and allow third-party apps to integrate with existing bank accounts. There are two types of open banking APIs: private and public APIs. The first is used for sharing data within the organization, while the latter is used for exchanging data with partners.

Open banking and APIs will play a major role in the future of banking, so those organizations in banking and finance should prepare and not just for regulatory reasons.

How does open banking and its APIs benefit banks and their customers?

These APIs, which have accelerated under open banking, allow third-party developers to integrate with a bank’s services and improve the customer experience, generating benefits for everyone involved.

Ability to launch new products and services faster — With the emergence of new technologies, customer expectations have increased, and banking companies have had to adapt to meet these new demands. For example, banks and fintech companies have been able to develop new products and services at a fast pace, and the use of APIs has allowed them to keep pace with this rapid evolution.

Increased customer engagement — APIs are also a useful solution for improving overall customer engagement. With the power to respond to customer requests in a fast, secure, and future-proof way, APIs enable banks to become more appealing to their customers. Banks can also use APIs to create more targeted offers based on customer information. Furthermore, APIs provide convenient access to the core services of banks, such as loan origination and servicing.

Ability to reach new customers — Financial service aggregator applications allow customers to make comparisons between offers and give customers access to products that were previously available only at branches, thanks to APIs. This fosters competition, and it also leads users to become customers of the banks that provide the APIs. Think loan rate and credit card comparison tools.

New revenue streams — In addition to building new products at a faster rate, 80% of banks charge customers a transaction fee to use the APIs. Revenue sharing with the ecosystem partner, such as a fintech, is another way banks are monetizing their APIs.2

Increased innovation through fintech collaboration — Banks and financial institutions can partner with fintechs to stay up to date with the latest technologies and figure out ways to use them to better serve customers and remain competitive.

What are the recent changes in open banking initiatives and mandates?

Along with the multitude of open banking benefits, regulations requiring banks to expose APIs to the public are a key step in making banking more open.

In the UK, for example, the Competition and Markets Authority (CMA) investigated the lack of competition in the retail banking industry and established the Open Banking Implementation Entity (OBIE), which develops open banking APIs, security architectures, and data structures that enable banks to share information with other financial services.

In the EU’s case, the Payment Second Payment Services Directive (PSD2) requires banks to allow certain third parties to access customer information (when given permission by the customer) and forces banks to implement certain security measures. The goal of PSD2 is to make payments more secure and to help with innovation.

Other countries also have their own regulatory initiatives when it comes to open banking. For instance, the Consumer Data Right (CDR), which gives consumers access to their banking data, is a regulatory initiative that kicked off in Australia in 2020.

Overall, 80 countries have instituted open banking regulations, and 75 countries are in the process of doing so.3

As for the US, there are currently no mandates for open banking. However, open banking is gaining ground here, driven by customer demand and the desire to do business in countries that do have such mandates.

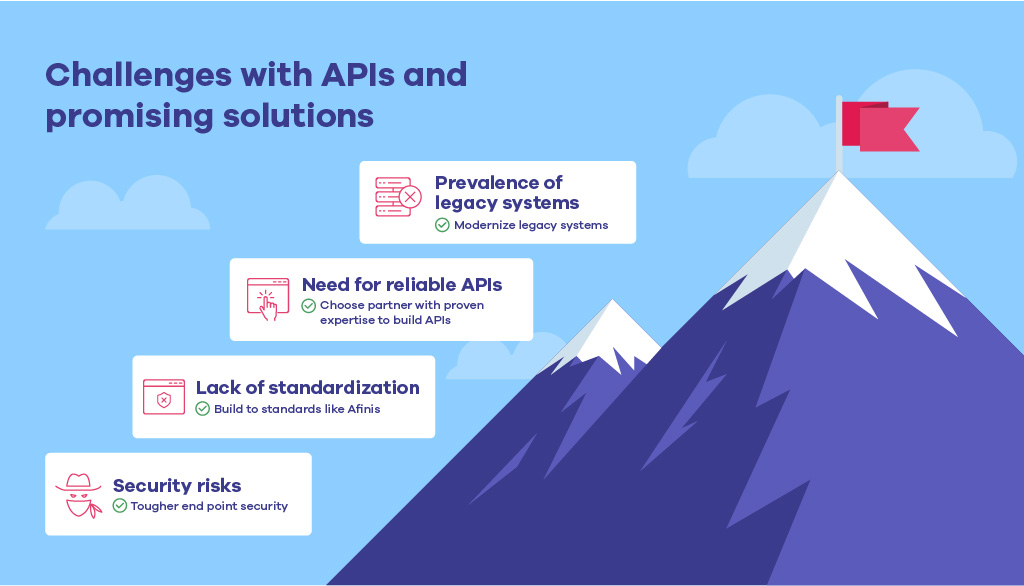

Challenges with APIs and promising solutions

Joining the open banking ecosystem through the use of APIs may offer many benefits, but implementing those APIs does come with some possible challenges. Here are some of those challenges as well as some promising solutions.

Prevalence of legacy systems — It’s understandable that organizations in the banking and finance sectors have held on to their legacy systems. These industries are highly regulated, so it’s important that any technology solution addresses all compliance and security requirements but these legacy systems have grown more and more complex and are keeping banks and financial institutions from implementing APIs effectively. In turn, the legacy systems are making it difficult for them to join the open banking ecosystem with the cloud’s many benefits and solutions geared toward security and compliance, now is the perfect time to modernize these legacy banking systems.

Need for reliable APIs — To gain all the benefits of open banking, the APIs used must be reliable and performant. Banking and finance organizations are relying on third parties to provide those APIs or to integrate with their own so that they can provide their customers with new features and improved user experiences but what if there’s an outage with one of those APIs? It can affect the entire application that’s using it and cause the customer experience to degrade instead of improve it’s therefore important for developers at these organizations to test these APIs and to do their research before implementing them to make sure they meet their performance and reliability standards.

Standardization — If an organization develops their own APIs and makes them available to other entities such as banks and software companies, they need to be sure all the systems can interface with each other. That can be difficult if everyone is using their own APIs they built in-house, with no standardization to address this, several organizations around the world have created standards to ensure that these APIs can interface with third parties.

One organization, Nacha, has a standardization group called Afinis. US firms such as Bank of America, Wells Fargo, Mastercard, and many more of the big players in finance have joined together to develop standardized, payment-related APIs. There are currently 18 APIs that are available for use.4

Security risks — Unfortunately, the more banks use APIs to share customer data, especially with third parties they can’t control, the more trouble banks will have in keeping that data secure.

Banks can answer this by controlling what is theirs, which includes making their own apps as secure as possible, as well as implementing tougher endpoint security. This means protecting their employee’s devices that they use to access that data.

Conclusion

Open banking is here to stay, whether that’s through mandates that arrive on US shores or customers who demand the features it provides. After all, APIs and open banking ecosystems will enable banks to customize the customer experience and improve customer retention and loyalty. At the same time, they allow for traditional financial institutions to stay at the center of customer data and financial relationships.

What Relevantz Can Do for You

Relevantz can be the partner you need for holistic cross-service model banking solutions that support core banking and other mission-critical applications. With our business-first, outside-in modernization approach, Relevantz can help your application modernization initiatives, including the rehosting, replatforming, refactoring, rearchitecting, rebuilding, and replacing of your current enterprise systems. We can also separate the applications from legacy infrastructure, modularize intermingled business processes, liberate data from legacy systems, and innovate new digital systems.

And because our approach is iterative, your enterprise will be able to enjoy all the benefits of new information technologies, such as having the agility to adapt quickly to the demands of the marketplace, while keeping your legacy systems humming behind the scenes.

https://www.gobankingrates.com/banking/banks/85-percent-people-prefer-banking-online-mobile-app-what-are-best-bets/

https://www.mckinsey.com/industries/financial-services/our-insights/from-tech-tool-to-business-asset-how-banks-are-using-b2b-apis-to-fuel-growth

https://fintechnews.ch/open-banking/open-banking-adoption-1578-banking-platforms-and-5564-apis-worldwide/54340

https://www.nacha.org/afinis-interoperability-standards